For the better part of the last decade, outsourcing fulfillment looked like the smart play. Third-party logistics providers offered scale, flexibility, and a way to convert fixed warehouse costs into variable ones. For many operators, it made sense.

That calculation is changing.

3PL fees have climbed steadily. SLA misses during peak periods have become harder to absorb. And as customer expectations around delivery speed, order accuracy, and returns experience have tightened, the gap between what operators can control and what they can influence through a third party has become a real business problem.

More operations leaders are asking the same question: is it time to bring fulfillment back in-house?

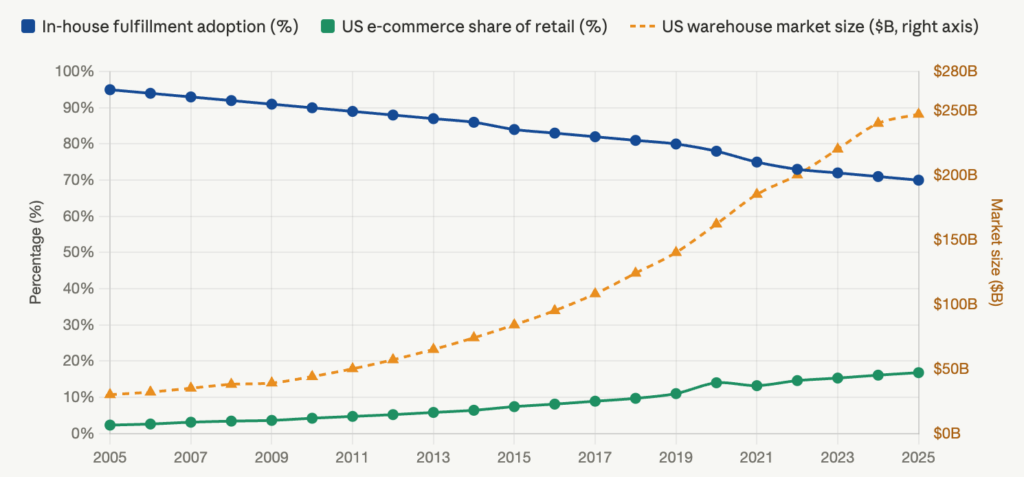

The data reflects this shift, and the chart below captures how the market has moved over the last two decades.

For many, the honest answer used to be no, not because in-house fulfillment wasn’t desirable, but because the trade-offs were too steep. Space, capital, labor, complexity. And for a long time, outsourcing absorbed that burden well enough.

But that drop in in-house fulfillment adoption did not happen because operators lost interest in control. It happened because the conditions made outsourcing fulfillment the easier path. Those conditions are now shifting and the operators who moved away from in-house fulfillment are starting to bring it back.

This blog is about what has changed, why in-house fulfillment is no longer as impractical as it once was, and what a realistic path back actually looks like.

The Business Case for In-House Fulfillment

Before the conversation turns to technology, it is worth being direct about why in-house fulfillment is worth reconsidering at all. The case is not simply about cost; it is about what operators gain back when they own the function.

- Fulfillment cost control. Variable 3PL pricing – per-pick, per-unit, per-pallet, compounds quickly at scale. Bringing fulfillment in-house converts unpredictable variable cost into a more manageable fixed-cost structure. For operations with stable or growing volumes, that shift meaningfully improves unit economics over a two-to-three-year horizon.

- Inventory visibility. When a third party holds your inventory, you are working off their data, on their timeline. Real-time, bin-level visibility – knowing exactly what you have, where it is, and how fast it is moving, becomes an internal capability when fulfillment is in-house. That visibility feeds better purchasing decisions, fewer stockouts, and faster resolution when something goes wrong.

- Customer experience. Delivery speed and accuracy are now expectations, not differentiators. Operators who control their own fulfillment control the last physical touchpoint with their customers. That means the ability to set and enforce their own SLAs, manage packaging and presentation, and respond to issues without waiting on a third party to investigate.

- Operational agility. The ability to react to a spike in demand, a new product launch, a returns surge – is significantly higher when fulfillment is internal. Outsourced operations require coordination, notice periods, and contractual flexibility that rarely matches the speed of real business decisions.

In-house fulfillment is not just a cost play. It is a strategic choice about which parts of the customer experience an operator is willing to own.

Wanting fulfillment in-house and being able to run it competitively are two different things. At meaningful order volumes, in-house fulfillment only matches 3PL economics when it’s automated. Manual picking can’t keep pace with today’s labor costs, or the throughput and accuracy customers expect. So, the real question was rarely whether to bring fulfillment in-house. It was whether the automation that makes in-house viable was worth its cost. For a long time, it wasn’t, and the case against it rested on three constraints: space, complexity, and labor.

Why the Old Barriers Are Being Reassessed

Space and capital commitment were the most tangible barriers. Traditional fixed-racking ASRS installations required purpose-built facilities, civil modifications, and multi-year infrastructure commitments. For operators in leased facilities, or those whose volume didn’t justify the footprint, the math simply didn’t work.

Complexity was the second barrier. Integrating automation with existing warehouse management systems, training staff, and managing a technology layer on top of an already demanding operation added real risk. Many operators who explored ASRS in earlier cycles found that the implementation burden exceeded what their teams could absorb.

Labor was often treated as a variable that could be managed: hire more during peak, reduce after. That assumption no longer holds for a significant portion of the market.

Labor availability and wage inflation are no longer cyclical problems for many operators. The combination of a persistently tight labor market and rising wages in key logistics corridors means that headcount-dependent fulfillment models carry structural cost risk that is not going away. Automation, in this context, is not just a productivity decision. It is a business continuity decision.

Operators who previously deferred automation because labor was manageable are now looking at a different risk profile. The question is not whether to reduce labor dependency, but how to do it without overcommitting to infrastructure that may not fit next year’s operation.

How Rapyuta ASRS Addresses In-House Fulfillment Specifically

Most automation vendors position around throughput and accuracy, and those metrics matter. But for an operator evaluating whether to bring fulfillment back in-house, the more important questions are: Can this fit in my existing facility? Can I start without a full warehouse redesign? And if my business changes, am I locked in?

Rapyuta ASRS was built on a different assumption: that most operators cannot and should not bet their entire operation on a single large-scale automation commitment. The system is designed to be flexible and modular in ways that are specific and operational, not just marketing language.

Here is what that means in practice.

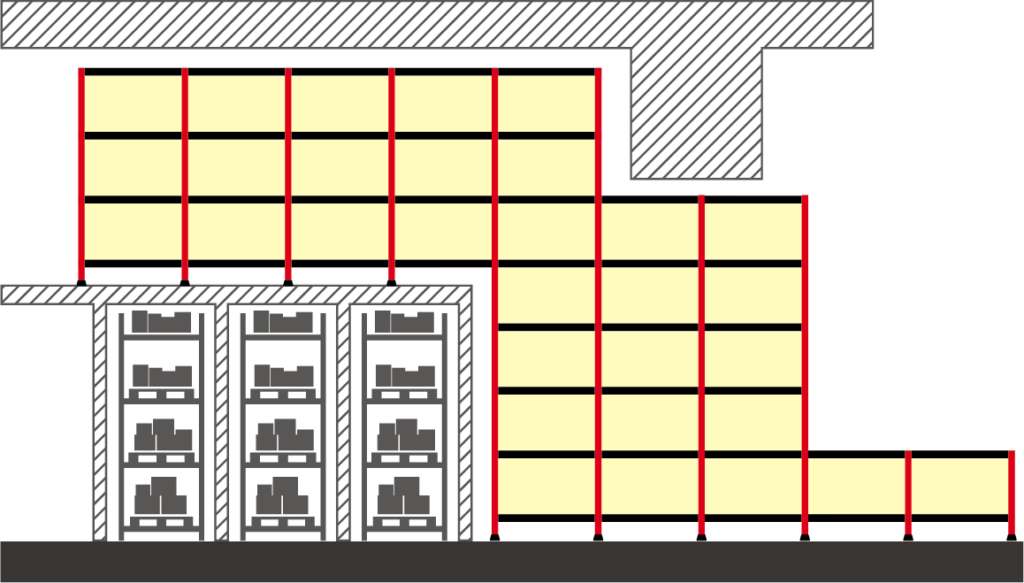

- It fits the space you have. The Rapyuta ASRS structure is anchorless and modular. It does not require permanent structural modifications, which means it can be deployed in leased facilities without triggering civil works. The vertical elevators can be positioned anywhere in the grid, not at fixed endpoints, which allows the system to work around columns, mezzanines, and irregular floor plans that traditional ASRS cannot accommodate. Operators do not need to find a better building. They can use the one they are in.

- It allows phased adoption. This is where Rapyuta’s approach diverges most clearly from the industry norm. Operators can deploy a partial system, covering a defined zone or SKU range, validate the throughput and ROI, and then expand. Modules can be added without shutting down the existing operation. There is no requirement to automate everything at once, which changes the risk calculus significantly for operators who are uncertain about volume projections or who want to learn before committing further.

- It does not lock the operator in. The system is relocatable. If the business outgrows the facility, changes its fulfillment strategy, or needs to redeploy capacity to a different site, the ASRS can be disassembled and moved. For operators weighing in-house against outsourcing, the ability to adapt the system as the business evolves removes one of the core risks that has historically made large automation commitments difficult to justify.

- It scales with demand, not against it. Adding capacity means adding modules, not redesigning the installation. The system can grow incrementally as order volumes increase and can be adjusted for seasonal patterns without requiring a separate 3PL overflow arrangement. For operations with significant peak-to-trough variation, this matters.

- It works within live operations. Installation, expansion, and reconfiguration can happen around an active fulfillment floor. Operators do not need to take downtime to deploy or grow the system. This removes a practical barrier that has caused many automation projects to stall at the evaluation stage.

The differentiator is not speed or accuracy – every credible ASRS vendor claims those. The differentiator is that operators can start small, prove the model, and expand on their own terms.

What Getting Started Actually Looks Like

The practical concern most operations leaders carry into an automation evaluation is not whether the technology works, it is what the transition looks like while the business is still running.

A phased approach to Rapyuta ASRS typically moves through a few distinct stages, though the specifics will vary based on facility, volume, and operational complexity.

- Assessment and simulation. Before any hardware commitment, operators can model expected throughput, space utilization, and ROI against their actual order data. This is a low-risk way to pressure-test assumptions and build an internal business case.

Try our ROI Calculator and see the numbers!

- Initial deployment in a defined zone. Rather than converting the full operation, the first installation typically covers a specific SKU range or order type, often fast-movers or high-volume SKUs where the throughput benefit is most visible. The rest of the operation continues as normal.

- Validate, then expand. Once the first zone is live and the team has operational confidence in the system, expansion decisions are made based on real data – actual pick rates, error rates, and labor impact, rather than vendor projections. Additional tiles and stations are added to the existing structure, scaling throughput without disrupting live operations.

The result is a transition that is operationally manageable and financially de-risked. Operators are not required to make a single large commitment and then hope the projections hold. They can learn, validate, and grow at a pace the business can absorb.

Which Operations Are Best Positioned for This

Not every fulfillment operation is at the right point to bring things in-house, and modular ASRS is not the right fit for every context. Being clear about where it does and does not make sense is more useful than a broad claim.

The strongest fits are driven by one or both of two economics: throughput andlabor, or storage density and space. An operation usually qualifies by being strong on at least one. The characteristics we tend to see:

- Order volumes meaningful enough to justify a dedicated fulfillment function, typically several hundred to several thousand orders per day.

- SKU ranges where a goods-to-person model adds genuine efficiency. Not single-SKU pallet movement, but multi-SKU environments where pick-path walking and search time represent real labor cost.

- Case-picking operations, where the system delivers full cases to the operator and removes the travel and search that dominate manual case pick. This is a particular strength of the platform, and it widens fit beyond piece-pick environments. Operations moving cases across many SKUs benefit even where each-level picking is light.

- Storage density as a constraint in its own right, whether from limited floor area, costly real estate, or SKU growth outpacing the current footprint. Consolidating storage into the cube frees usable space even when throughput is modest.

- Facilities that are leased or structurally constrained, where deploying without civil works or permanent modification is necessary and not just convenient.

- Businesses under labor cost pressure or availability issues, where the automation decision is tied to workforce risk and not just throughput targets.

- Operations with growth plans or demand variability, where a system that scales incrementally is more appropriate than a fixed installation sized for peak.

Equally, the timing may not be right for operators who are at very low volumes and have no density or space pressure to solve, who run purpose-built facilities already configured for fixed ASRS, or whose outsourcing arrangements are genuinely performing well. Low volume on its own is not disqualifying. A small operation that needs density can still be a strong fit, as long as the space economics justify the system. The goal is fit, not conversion.

The Shift Worth Paying Attention To

The conversation around in-house fulfillment is changing, not because the desire for control is new, but because the conditions that made outsourcing the pragmatic choice are eroding.

Rising 3PL costs, tightening labor markets, and higher customer expectations are converging at the same moment that automation technology has become more accessible, more flexible, and less demanding in terms of infrastructure commitment. That is not a coincidence; it is why the question of in-house fulfillment is back on the table for operators who had settled it years ago.

The historical trade-off between control and scalability was real. Running in-house fulfillment meant accepting a ceiling on how fast you could grow and how much you could flex. Modular, phased automation changes that trade-off. Operators can now have meaningful control over their fulfillment operation without accepting the rigidity that control used to require.

That is the shift worth watching. Not the automation itself, but the fact that the barriers that made outsourcing the default choice are no longer as fixed as they appeared.

For operators reconsidering where fulfillment sits in their business, the question is no longer whether in-house is viable. The question is what a sensible first step looks like, and whether the system they choose can grow with them if the answer turns out to be yes.